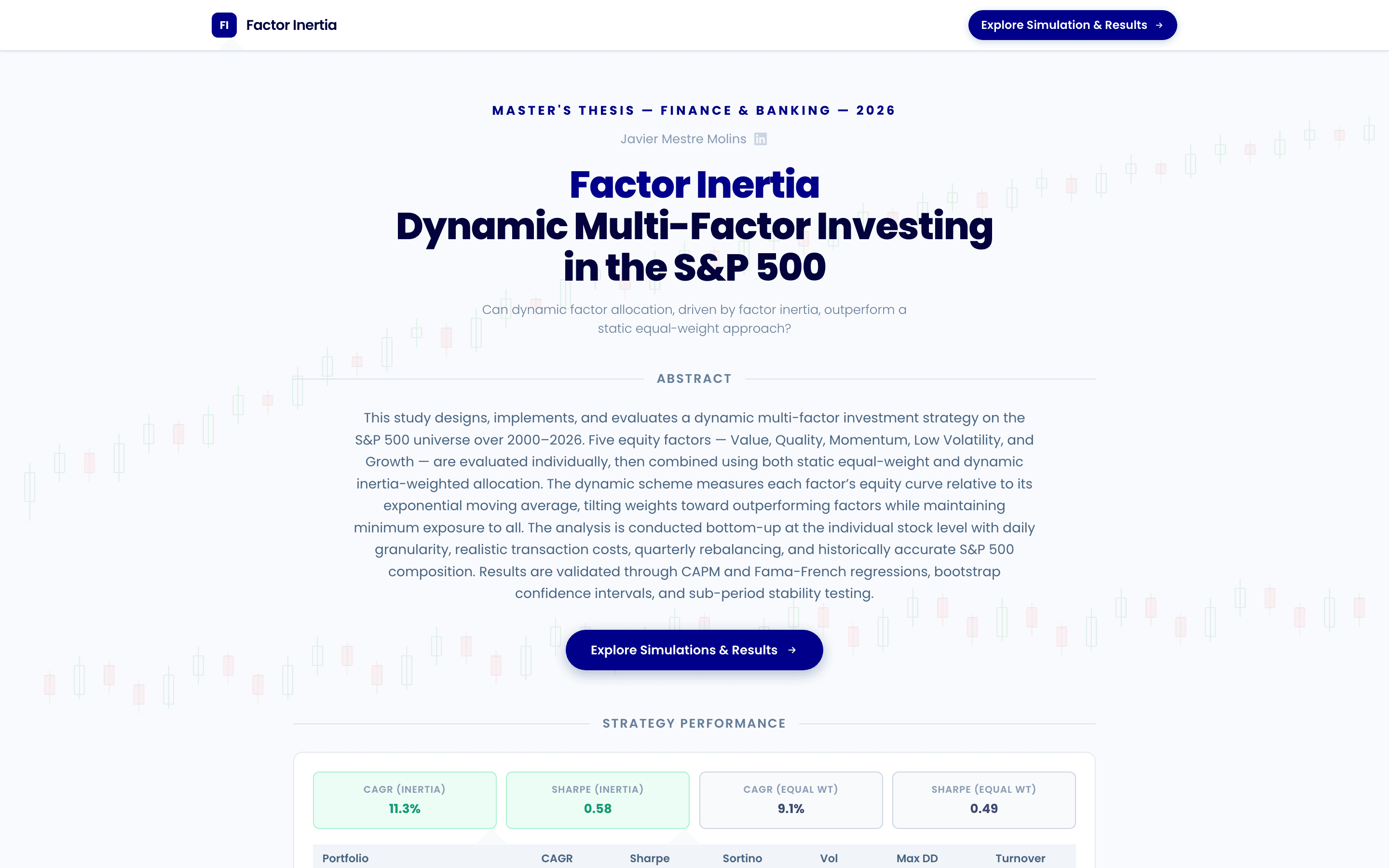

Featured · Quant2026

Factor Inertia: Dynamic Multi-Factor Investing in the S&P 500

A multi-factor S&P 500 strategy that uses factor inertia to tilt allocation toward the factors that are outperforming — Value, Quality, Momentum, Low Volatility and Growth — benchmarked against a static equal-weight approach.